5 Things to Know About GST Audit by Tax Authorities

1. What is GST Audit?

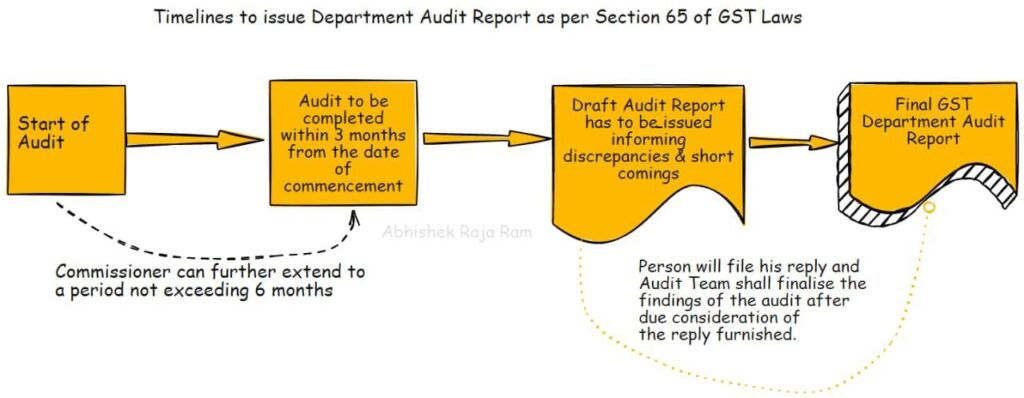

As per Section 65 of CGST Act 2017, The Commissioner or any officer authorized by him may undertake an audit of any registered person for such period, at such frequency and in such manner as may be prescribed.

Audit means the examination of records, returns and other documents maintained or furnished by the registered person under this Act to verify the correctness of turnover declared, taxes paid, refund claimed, and input tax credit availed, and to assess compliance with the provisions of this Act or the rules made thereunder.

2. What happens during the course of a GST Audit

The GST Audit process includes the following steps:

- The taxpayer is formally notified of an upcoming audit through the prescribed format (FORM GST ADT-01) at least 15 working days prior to the conduct of audit.

- FORM GST ADT-01 also enlists the documents and data to be submitted to the Auditor for a preliminary review. A period of 15 days is prescribed for submission of the documents.

- The audit will officially commence when the auditor accepts the documents submitted by the taxpayer or initiates verification of the business premises, whichever is later.

- During the audit, the authorized officer may request access to verify the books of accounts or other necessary documents. The taxpayer’s cooperation is crucial for a timely completion of audit.

- On completion of the audit verification, taxpayer receives the preliminary findings, and his views/comments are recorded to finalize the observations.

- On finalization of observations, the results are sent to the taxpayer in the form of Final Audit Report (Form GST ADT-02) within 30 days.

- The taxpayer is given the option to make the payment of tax short paid / not paid with waiver of show cause notice. The final audit findings are informed to the taxpayer within 30 days along with his rights and obligations and the reasons for such findings.

- The entire audit process is to be completed within 3 months from the date of commencement, with the provision of a further 6-month extension, if necessary, after prior approvals of higher authorities.

- If the GST Audit results in detection of tax being unpaid or short paid or erroneously refunded, or input tax credit wrongly availed or utilised, the concerned officer provides opportunity to pay the tax. If the taxpayer disagrees or does not pay the tax, GST Audit officer will move the case to a Jurisdictional officer to initiate the proceedings under section 73/74 of CGST Act 2017.

3. Some useful tips for taxpayers

- Take advantage of the laws under section 50 of CGST Act with respect to ITC wrongly availed but not utilised to avoid paying interest.

- Conduct timely reconciliation of records

- Compare e-Way Bills with respect to data in GSTR-1

- Compare GSTR-3B Returns filed, with GSTR-2B and GSTR-1, and ensure that all data matches

- Have a clear understanding of the provisions of CGST Act and Rules, invest your time to read it.

- Ensure timely filing of GSTR-9/9C return (whichever is applicable).

- Consult an experienced GST Professional for advisory services when faced with a GST Audit.

4. Benefits of audit to taxpayers

Participating in GST Audits offers several benefits for the taxpayer:

- Avoid penalties: Audit can help taxpayers to rectify the default in compliances with respect to tax not paid or short paid or erroneously refunded, or input tax credit wrongly availed or utilised without penalty under section 73 or with lesser penalty under section 74.

- Enhanced Compliance: Taxpayer gains a better understanding of tax laws and procedures, making compliance smoother.

- Precision in Returns: Taxpayer’s GST returns, and Self-assessments are prepared accurately, with a sharper focus on correctness and completeness.

- Improved Accounting: Audits can help taxpayers in spotting and rectifying deficiencies in accounting and internal control systems.

• Fewer Hassles: With thorough audits, the chances of disputes and legal proceedings decrease significantly.

5. Some important FAQs on audit by tax authorities under GST

FAQ’S

This blog is written by A.Yuvakiran working in V Ramaratnam and company