Received a Notice from the Income Tax Department for Foreign Income? Here’s What NRIs Need to Know

Many Non-Resident Indians (NRIs) working abroad earn various types of income outside India, including salary income, capital gains, investment income, or other foreign income. Based on their residential status under the Income Tax Act, such foreign income may not be taxable in India.

Many NRIs are now receiving an Indian income tax notice for foreign income reported in their income tax returns. If you have received such a notice, there is no need to panic. In most cases, the Department is simply requesting an explanation and supporting documents to verify the information disclosed in your return.

Consider a common situation:

An individual worked abroad for several years and later returned to India. After returning, he transferred his overseas savings, including salary and investment income earned while living abroad — say $100,000 — to his Indian bank account. Since the income was earned outside India during his stay overseas, he believed it was not taxable in India. Later, he received a notice from the Income Tax Department asking him to explain the source of funds credited to his account and provide documents supporting his claim that such income is non-taxable.

Understanding why such notices are issued and how to respond is important for anyone moving between countries.

Importance of Determining Residential Status Correctly

Residential status is one of the most important factors in determining tax liability. A person may be classified as:

- Resident and Ordinarily Resident (ROR)

- Resident but Not Ordinarily Resident (RNOR)

- Non-Resident (NR)

The tax implications differ significantly for each category. Many tax disputes arise because taxpayers incorrectly determine their residential status. An individual who assumes he is a non-resident but actually qualifies as a Resident may inadvertently omit income that is taxable in India.

Accordingly, maintaining records such as passport copies, immigration records, visa details, travel history, and employment contracts is crucial to establishing the correct residential status.

Taxability of Foreign Income for NRIs

A common misconception is that all income earned abroad is automatically exempt from tax in India. The actual tax treatment depends on several factors, including residential status, source of income, place of accrual, and place of receipt.

For a person qualifying as a Non-Resident under the Income Tax Act, the taxability of income is as follows:

- Income received or deemed to be received in India is taxable in India.

- Income accruing or arising in India is taxable in India.

- Foreign income earned outside India and received outside India is generally not taxable in India.

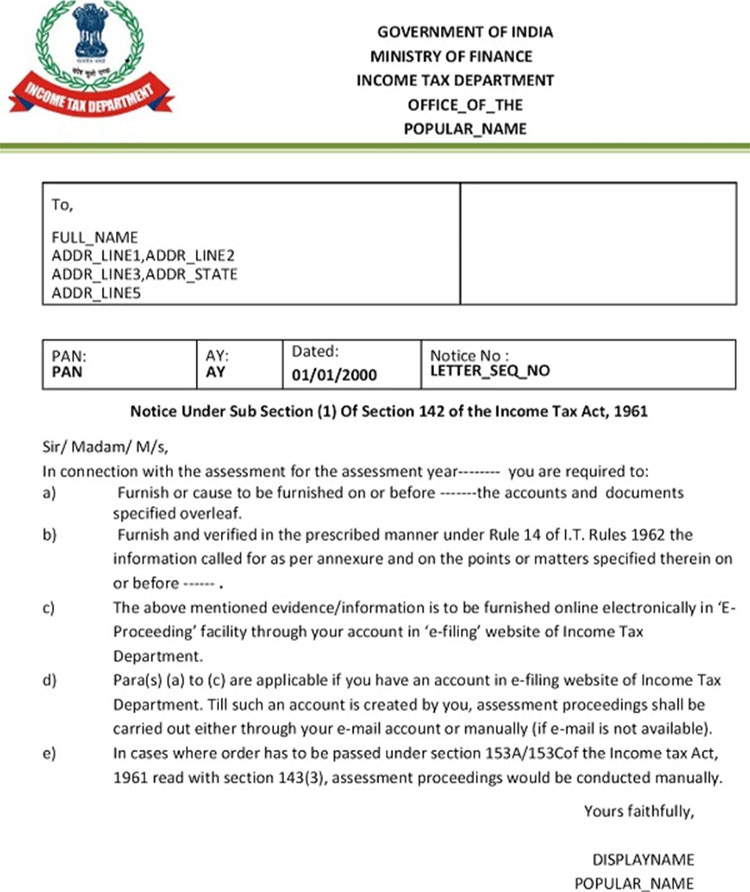

What is a Notice under the Income Tax Act?

This section explains the meaning of a notice under income tax, its purpose, and the appropriate way to respond.

Instances where a notice may be issued:

- The Department requires supporting evidence regarding residential status.

- There is a mismatch between information available with the Department and disclosures made in the return.

- The taxpayer has disclosed significant foreign income but has not adequately explained its tax treatment.

- Certain foreign transactions require verification.

- The taxpayer did not report foreign income or overseas assets, where required.

- The Department seeks additional documents during assessment proceedings.

Therefore, receiving a notice should not automatically be viewed as a sign of non-compliance. In many cases, it forms part of the routine verification process.

[Sample of a Notice under the Income Tax Act]

How to Respond to a Notice

The response should be comprehensive and supported by documentary evidence. Ignoring a notice or providing incomplete information may result in unnecessary complications and prolonged proceedings. The response should include the following points:

Residential Status

The taxpayer should demonstrate why he qualifies as a Non-Resident or Resident but Not Ordinarily Resident for the relevant financial year. Supporting documents may include passport copies, travel records, employment contracts, visa documents, and residency permits.

Nature of Income

The response should clearly describe the nature of the foreign income — whether it represents salary, business income, investment income, capital gains, dividends, interest, or any other category.

Source of Income

The taxpayer should identify the source from which the income was earned and explain how and where the income originated.

Place of Accrual and Receipt

A detailed explanation should be provided regarding where the income accrued and where it was received. This is often a critical factor in determining taxability.

Legal Basis for Non-Taxability

The response should refer to the relevant provisions of the Income Tax Act supporting the claim that the income is not taxable in India.

Supporting Documentation

Documents commonly submitted include:

- Passport copies

- Visa and immigration records

- Employment agreements

- Salary certificates

- Foreign tax returns

- Foreign tax payment receipts

- Overseas bank statements

- Tax Residency Certificates, where applicable

- Investment statements and transaction records

Once adequate supporting documentation and explanations are provided, the matter can generally be resolved satisfactorily.

Common Mistakes Made by NRIs

- Wrong Residential Status Calculation — Incorrect determination of residential status can result in incorrect tax treatment.

- Not Reporting Foreign Income — Many NRIs assume that non-taxable income need not be disclosed, which may invite scrutiny.

- Assuming All Foreign Income Is Automatically Exempt — Different categories of foreign income may have different tax implications.

- Ignoring Tax Notices — Failure to respond within the prescribed timeline can lead to adverse consequences.

- Inadequate Documentation — Insufficient records often make it difficult to substantiate claims during assessment proceedings.

Conclusion

Being aware of your tax responsibilities and replying to income tax notices within the prescribed time is essential for addressing any concerns raised by the tax authorities. This not only helps resolve matters promptly but also supports long-term compliance through accurate and proper tax filings.